Rate Buydown Loan Options

A rate buydown can help reduce the interest rate on a mortgage, either for a temporary period or for the life of the loan. Depending on the structure, a rate buydown may help lower the monthly payment during the first few years of the loan or reduce the interest rate permanently for long-term savings.

There are two common types of rate buydown options:

Temporary rate buydown

Permanent rate buydown

The right option depends on your goals, cash available, seller credits, builder incentives, and how long you expect to keep the loan.

Rate Buydown Options May Help You:

Lower your starting monthly payment

Use seller credits or builder incentives strategically

Improve short-term affordability

Reduce the interest rate permanently

Compare upfront cost versus long-term savings

What Is a Rate Buydown?

A rate buydown is a mortgage strategy where money is paid upfront to reduce the borrower’s interest rate.

That upfront cost may be paid by:

the borrower

the seller

the builder

another eligible interested party, depending on loan program guidelines

A buydown can be structured as either a temporary buydown or a permanent buydown.

The key difference is simple:

A temporary buydown lowers the payment for a limited period.

A permanent buydown lowers the interest rate for the life of the loan.

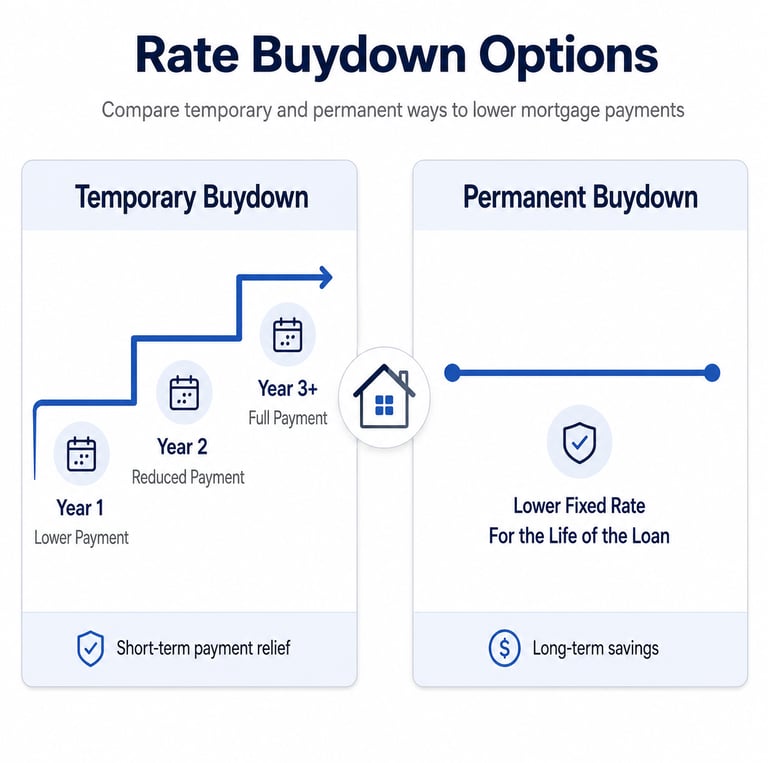

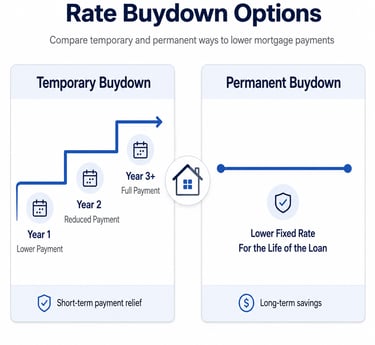

Temporary Rate Buydown

What Is a Temporary Rate Buydown?

A temporary rate buydown lowers the borrower’s monthly payment for the first part of the loan term. The note rate does not permanently change, but funds are set aside in a buydown account to subsidize the payment during the temporary buydown period.

Common temporary buydown structures include:

3-2-1 buydown

2-1 buydown

1-0 buydown

The most common option is a 2-1 temporary buydown, where the borrower’s effective payment is reduced for the first two years.

Example: 2-1 Temporary Buydown

With a 2-1 temporary buydown, the borrower’s payment is temporarily reduced during the first two years.

Example structure:

Year 1: payment is based on a rate 2% lower than the note rate

Year 2: payment is based on a rate 1% lower than the note rate

Year 3 and after: payment is based on the full note rate

This can help a borrower ease into the full mortgage payment, especially if they expect income to increase, expenses to change, or plan to refinance later if market rates improve.

Example: 3-2-1 Temporary Buydown

With a 3-2-1 temporary buydown, the payment is reduced for the first three years.

Example structure:

Year 1: payment is based on a rate 3% lower than the note rate

Year 2: payment is based on a rate 2% lower than the note rate

Year 3: payment is based on a rate 1% lower than the note rate

Year 4 and after: payment is based on the full note rate

This option can create a larger temporary payment reduction, but it also usually requires more upfront funds to cover the buydown cost.

When a Temporary Rate Buydown May Make Sense

A temporary rate buydown may be useful when:

the seller or builder is offering credits

the buyer wants a lower starting payment

the borrower expects income to increase

the buyer wants short-term payment relief

the borrower believes refinancing may be possible later

the goal is to improve early cash flow after buying a home

Temporary buydowns are especially common when sellers or builders want to offer an incentive without reducing the purchase price.

Temporary Buydown Warning

A temporary buydown should not be confused with a permanent lower rate.

The borrower must be able to qualify for and afford the full payment after the temporary buydown period ends. If the payment is reduced for the first one, two, or three years, the borrower should still understand what the payment becomes when the full note rate applies.

This is where a lot of buyers make bad decisions. They focus on the starting payment and ignore the future payment.

Permanent Rate Buydown

What Is a Permanent Rate Buydown?

A permanent rate buydown lowers the mortgage interest rate for the life of the loan by paying discount points or other eligible upfront costs at closing.

Unlike a temporary buydown, a permanent buydown does not expire after one, two, or three years. The lower rate remains in place for as long as the borrower keeps that loan.

This may help reduce:

monthly payment

total interest paid over time

long-term borrowing cost

How Discount Points Work

A permanent buydown is often done by paying discount points.

One discount point typically equals 1% of the loan amount. For example, on a $400,000 loan, one point would cost $4,000.

The exact rate reduction from paying points depends on market pricing, loan type, credit profile, occupancy, loan amount, and other factors. Points do not always reduce the rate by the same amount, so the cost should be compared carefully.

When a Permanent Rate Buydown May Make Sense

A permanent rate buydown may be useful when:

the borrower plans to keep the loan for a long time

the long-term interest savings outweigh the upfront cost

seller credits are available and need to be used strategically

the buyer wants a lower monthly payment for the life of the loan

the borrower wants more predictable long-term savings

A permanent buydown is usually more attractive when the borrower expects to keep the home and mortgage long enough to recover the upfront cost.

Break-Even Point

The most important question with a permanent rate buydown is:

How long does it take to recover the upfront cost?

This is called the break-even point.

Example:

If the permanent buydown costs $4,000

And it saves $100 per month

The break-even point is about 40 months

If you sell or refinance before reaching the break-even point, the buydown may not have been worth it. If you keep the loan longer than the break-even point, it may create real savings.

Temporary vs Permanent Rate Buydown

Both options can reduce payment, but they work differently.

Temporary Rate Buydown

A temporary buydown:

lowers the payment for a limited time

usually lasts 1 to 3 years

does not permanently reduce the note rate

is often funded by seller or builder credits

can help with short-term affordability

requires understanding the future full payment

Permanent Rate Buydown

A permanent buydown:

lowers the actual interest rate for the life of the loan

is often paid through discount points

may be funded by borrower funds, seller credits, or builder incentives

can reduce long-term interest cost

works best when the borrower keeps the loan long enough to break even

Seller Credits and Builder Incentives

Seller credits and builder incentives can often be used to help pay for rate buydown options, depending on the loan program and transaction structure.

This can be useful because a seller or builder credit may allow the borrower to lower the payment without using as much of their own cash at closing.

Possible uses may include:

temporary rate buydown

permanent rate buydown

closing costs

prepaid items

other allowable costs depending on loan program guidelines

The best use of credits depends on the borrower’s goals. Sometimes a temporary buydown makes sense. Other times, a permanent buydown or closing cost credit may be better.

Which Buydown Option Is Better?

The better option depends on the borrower’s financial goals.

A temporary buydown may be better if the borrower wants a lower payment early in the loan and has seller or builder credits available.

A permanent buydown may be better if the borrower wants long-term payment savings and expects to keep the loan long enough to justify the upfront cost.

A borrower should compare:

upfront cost

monthly payment savings

break-even point

seller or builder credits available

expected time in the home

likelihood of refinancing

long-term interest savings

Rate Buydown FAQs

What is a rate buydown?

A rate buydown is a mortgage strategy where funds are paid upfront to lower the borrower’s mortgage payment or interest rate, either temporarily or permanently.

What is a temporary rate buydown?

A temporary rate buydown lowers the borrower’s payment for a limited period, often the first one, two, or three years of the loan.

What is a permanent rate buydown?

A permanent rate buydown lowers the interest rate for the life of the loan by paying discount points or other eligible upfront costs.

What is a 2-1 buydown?

A 2-1 buydown typically lowers the borrower’s effective payment by 2% in year one and 1% in year two. In year three, the payment is based on the full note rate.

What is a 3-2-1 buydown?

A 3-2-1 buydown typically lowers the borrower’s effective payment by 3% in year one, 2% in year two, and 1% in year three. In year four, the payment is based on the full note rate.

Can seller credits be used for a rate buydown?

Yes, seller credits may be used for rate buydown options, subject to loan program guidelines and interested party contribution limits.

Can builder incentives be used for a rate buydown?

Yes, builder incentives may be used for rate buydowns when allowed by the loan program and transaction structure.

Is a temporary buydown the same as a lower fixed rate?

No. A temporary buydown only reduces the payment for a limited time. The borrower must understand the full payment that applies after the buydown period ends.

Is paying points always worth it?

No. Paying points only makes sense if the monthly savings and time kept in the loan justify the upfront cost.

Which is better: temporary buydown or permanent buydown?

It depends on the borrower’s goals. Temporary buydowns help with short-term payment relief, while permanent buydowns may help with long-term savings.

Contact

Armstrong Mortgage LLC – NMLS #2444347 Equal Housing Opportunity

Phone

michael@armstrongmtg.com

317-362-6346

© 2025. All rights reserved.

Michael Armstrong – NMLS #1623098

Important Disclosures

Program guidelines, rates, terms, and availability are subject to change without notice. All loans are subject to credit approval, underwriting review, property eligibility, collateral review, title review, and applicable program guidelines. Stated guidelines are not a commitment to lend. Meeting minimum credit score, down payment, reserve, acreage, and loan amount requirements does not guarantee approval. Rates are subject to market conditions and borrower qualifications. Call for current rate information based on your specific loan scenario. Additional restrictions may apply.